For decades, the landscape of professional sports ownership has been strikingly uniform: predominantly white, predominantly male, predominantly inherited wealth. Meanwhile, the leagues themselves — the NFL, NBA, and WNBA in particular — have been powered overwhelmingly by Black athletes. The disconnect has been glaring and well-documented. But a quiet revolution is underway, and it's being led not by the players, but by a new generation of Black financiers, media moguls, and executives who are buying seats at the table.

The 2024-2025 NFL season made history with the highest number of Black minority team owners in the league's history. It's a milestone worth celebrating — and worth examining, because the people driving that change are as compelling as the change itself.

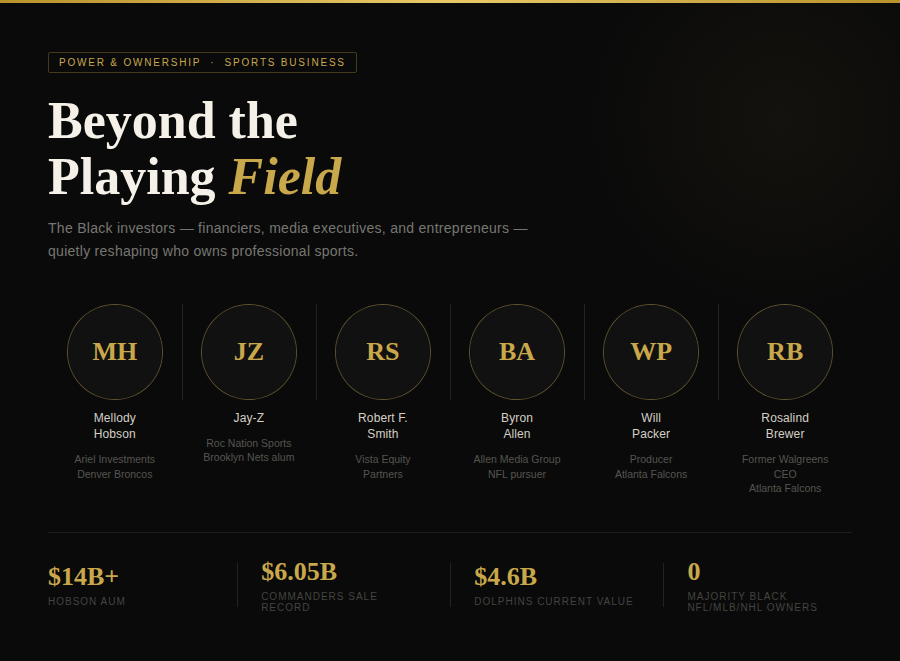

Mellody Hobson — The Trailblazer in the Boardroom

If there's one name that anchors this conversation, it's Mellody Hobson.

The co-CEO and President of Ariel Investments — one of the largest Black-owned asset management firms in the United States, with over $14 billion in assets under management — Hobson has spent decades navigating financial power structures that were not designed for her. In June 2022, she made history again: joining the ownership group that purchased the Denver Broncos for a record $4.65 billion, becoming the first Black woman to hold an ownership stake in an NFL franchise.

The significance wasn't lost on Broncos quarterback Russell Wilson at the time, who called it "history-making" and noted it had perhaps "gone over people's heads a little bit." Hobson didn't just buy a sliver of a football team — she bought it as a financial institution builder, an investment professional, and a woman who has sat on the boards of Starbucks and JPMorgan Chase. This wasn't celebrity ownership. This was institutional capital meeting professional sports.

And she isn't stopping there. Through Project Level, Ariel Investments' women's sports-focused fund, Hobson has raised $250 million to invest across the women's sports ecosystem — from franchise ownership to the technology and infrastructure that surrounds it. Her position is clear: women's sports aren't an "emerging story" anymore. Their time has arrived, and she intends to be at the center of it.

Jay-Z — The Blueprint Maker

Long before he became a mogul in the traditional business sense, Shawn Carter — Jay-Z — was writing the blueprint for Black investment in professional sports.

In 2003, he invested approximately $1 million for a minority stake in the New Jersey Nets, becoming one of the most prominent Black investors in professional sports at the time. His involvement went beyond a financial check: he was integral to the Nets' rebrand and relocation to Brooklyn, helping transform the franchise's identity and fanbase. It was a proof of concept — that hip-hop culture, Black business acumen, and sports investment could occupy the same space.

He sold his Nets stake in 2013, but for a reason that only deepened his influence in sports: to launch Roc Nation Sports, a full-service athlete representation and management agency that has grown into one of the most powerful in the world, with a roster spanning the NFL, MLB, NBA, and international football. Roc Nation didn't just manage athletes — it reimagined what a sports agency could be, building brands, media partnerships, and cultural capital alongside traditional contracts.

Jay-Z's pivot from team ownership to sports infrastructure may have been the more powerful move. Owners come and go. The agency that shapes athletes' careers, images, and deals has longer, quieter leverage.

Venus & Serena Williams — Pioneers in the NFL

Before we move further, it's worth pausing on the Williams sisters — not as athletes here, but as investors and pioneers of a different kind.

In 2009, Venus and Serena Williams became the first Black women to hold ownership stakes in an NFL franchise, purchasing a minority interest in the Miami Dolphins. At the time, the team was valued at approximately $1.02 billion. Today, that valuation sits around $4.6 billion — a return that speaks for itself.

The investment was historic, visionary, and — perhaps most importantly — early. They didn't wait for the door to open wider. They walked through the one that existed and, in doing so, helped widen it for everyone who came after.

Will Packer — Hollywood Meets the Huddle

Will Packer is one of Hollywood's most successful film producers, responsible for hits including Girls Trip, Straight Outta Compton, and Think Like a Man. In May 2024, he expanded his footprint significantly by joining the Atlanta Falcons' ownership group as a limited partner — alongside Rosalind Brewer, Rashaun Williams, and Olympic champion Dominique Dawes.

Falcons owner Arthur Blank described the group as "impressive leaders who have made an impact in a variety of enterprises." For Packer specifically, the ownership stake represents a bridge between entertainment and sports — two industries that have been converging for years, but where Black ownership has historically remained on the entertainment side of the ledger. Packer's Falcons investment puts him in the room where stadium deals, broadcast rights, and franchise strategy get decided.

Rosalind Brewer — The Executive in the Owner's Suite

Joining Packer in the Atlanta Falcons ownership group, Rosalind Brewer brings a distinctly corporate C-suite pedigree to sports ownership. A former CEO of Walgreens Boots Alliance and COO of Starbucks, Brewer is one of a small number of Black women to have led a Fortune 500 company. Her addition to the Falcons' ownership group in 2024 signals a maturing of the Black investor class in sports — it is no longer only entertainers and athletes (or former athletes) buying in. It is executives, operators, and institutional thinkers.

Robert F. Smith — The One Who Almost Bought the Broncos

Robert F. Smith, the founder of Vista Equity Partners and the first Black American to sign the Giving Pledge, represents the ceiling of Black financial achievement in the United States. His firm manages over $90 billion in assets. He is, simply, one of the most powerful private equity investors in the world.

Smith was among the names reported to be actively pursuing the Denver Broncos before the franchise was ultimately sold to the Walton-Penner group in 2022. That he didn't land the Broncos is a story about how capital alone doesn't guarantee entry into the NFL's ownership club — networks, relationships, and league approval all play their parts. But Smith's pursuit was significant. It demonstrated that the capital to pursue majority NFL ownership exists within the Black investor class. The structural barriers that remain aren't about money.

Smith's presence in the sports investment conversation continues. As leagues increasingly court institutional investors, the Vista Equity playbook — patient capital, operational improvement, long-term value creation — maps well onto franchise ownership models.

Byron Allen — Media, Sports, and the Long Game

Byron Allen, the founder and CEO of Allen Media Group, has been one of the most persistent and vocal advocates for Black ownership in major professional sports. He made bids for both the Denver Broncos and the Washington Commanders (now the Commanders), only to see both deals go elsewhere. His media empire — which includes The Weather Channel, The Grio, and a portfolio of local television stations — gives him the kind of cross-platform reach that makes him a uniquely valuable potential sports owner in the media rights era.

Allen has been outspoken about what he sees as structural barriers to Black ownership in the NFL, and his continued pursuit of franchise ownership represents a principled, long-term campaign. The story isn't over. The Commanders deal that went to the Josh Harris group in 2023 — a record $6.05 billion transaction that included Magic Johnson as a minority owner — was another moment where Allen was edged out. But he remains one of the most credible Black voices pushing on the door of majority ownership.

The Bigger Picture

The individuals profiled here are not a monolith. They span finance, film, media, and tech. Some hold minority stakes; others are pursuing majority control. Some came through entertainment; others climbed corporate ladders. What they share is a willingness to direct capital toward an asset class — professional sports — that has historically treated Black wealth as labor, not ownership.

Across the NFL, NBA, MLB, and NHL's combined 154 franchises, zero teams are majority-owned by African Americans in the NFL, MLB, or NHL. That structural reality makes every minority stake, every limited partnership, and every bid for a franchise not just a financial decision, but a statement about where Black wealth is going and what it demands.

The playing field has always had Black excellence. The owner's suite is starting to catch up.